Field Notes Week 179/520: Reorganise, Automate, Build.

These notes are shaped by what I’m seeing, building, and discussing as our physical and digital lives continue to converge.

Welcome to this week’s Field Notes, a 10-year project of mine documenting humankind’s digital transition from the field. These notes are shaped by what I’m seeing, building, and discussing as our physical and digital lives continue to converge.

- Ryan

(Connect with me on LinkedIn)

News is surface-level. Signals live underneath. This section captures developments that hint at deeper shifts in how digital systems are being built, governed, and adopted — often before they’re obvious in the mainstream narrative.

News & Signals

Three stories this week suggest that some of the most revealing technology signals are no longer coming from product launches.

They are showing up in the operating systems around the products. Inside the workplace. Inside the store. Inside the national infrastructure stack. Meta’s plan to capture employee activity for AI training turns the labour process itself into data. Starbucks’ decision to scrap an AI inventory tool is a reminder that everyday operations remain harder to model than the demos suggest. And SoftBank’s €45 billion AI data-centre plan for France shows how quickly the centre of gravity has moved from models to land, power, and physical capacity.

Meta is pushing AI training deeper into the workplace

Reuters reported in April that Meta is installing tracking software on U.S.-based employees’ computers to capture mouse movements, clicks, and keystrokes for use in training its AI models, part of a broader push to build agents that can perform work tasks autonomously. Privacy lawyers told Reuters the practice could run into serious problems under EU workplace-surveillance rules if data from Europe or from EU-based staff were implicated.

What stood out is not only the privacy issue. It is the change in posture. Training data is no longer treated as something gathered from the outside world alone. It is increasingly something extracted from work itself. The internal operation of the company becomes part of the raw material for building the next generation of systems. That changes the feel of the AI story. Less public internet. More instrumented labour.

The deeper signal is that the boundary between software and workplace governance is getting thinner. Once employee activity becomes useful training input, questions about surveillance stop being side issues and start becoming part of the system design itself. That feels directionally important because it suggests the next phase of AI development may depend as much on what firms can observe about their own workers as on what they can scrape from the web.

Starbucks found the limits of operational AI the hard way

Reuters reported on 21 May that Starbucks scrapped its AI-based inventory tool across North America just nine months after rollout because it repeatedly misidentified products and failed to generate reliable stock counts. The tool, developed by NomadGo, used cameras and lidar on tablets to automate inventory checks. Starbucks is now reverting to manual counting while focusing on simpler daily replenishment routines.

What stood out here is how ordinary the failure was. Not a dramatic safety breach. Not a frontier model collapse. Just a worker-facing operational tool meeting the messy reality of a store and not holding up. That matters because so much of the AI conversation still centres on capability in isolation. Starbucks is a useful reminder that capability does not automatically survive contact with routine work, visual ambiguity, changing stock layouts, and the need for dependable execution.

The signal underneath it is that retail remains a harsher test environment than product demos suggest. The value of automation depends less on whether a tool can work in principle and more on whether it can work predictably, cheaply, and without adding new friction to already pressured frontline operations. In that sense, this is less a story about Starbucks and more a story about the difference between model performance and operational reliability.

France is becoming a test case for AI infrastructure as industrial policy

Reuters reported today that SoftBank plans to invest €45 billion over five years to build AI data centres in France, with the first three sites expected to deliver 3.1 gigawatts of capacity by 2031 and potential expansion taking the total to €75 billion and 5 gigawatts. Schneider Electric will supply modular solutions, while EDF is contributing a former power plant for conversion into a data-centre site.

What stood out is that this is no longer mainly a software story. It is a land, power, and industrial-location story. France’s attraction here is not just policy enthusiasm. Reuters says Masayoshi Son cited France’s energy production and export capabilities as decisive. That is worth noting because it shows how AI infrastructure decisions are increasingly being made on the basis of electricity, transmission, and conversion capacity rather than talent or model prestige alone.

The broader signal is that AI is starting to look more like heavy industry. Once projects are measured in gigawatts and tens of billions of euros, they start to reshape national planning, utility strategies, and industrial geography. The conversation moves from intelligence in the abstract to where the substations, land parcels, and financing structures will come from. That is usually the point at which a technology stops feeling speculative and starts becoming structural.

What stood out

Taken together, these stories suggest that AI is becoming harder to keep abstract.

At Meta, it reaches into the labour process. At Starbucks, it runs into the stubborn mess of daily operations. In France, it turns into an infrastructure buildout measured in power and capital. Different settings, same direction: the technology is moving out of the lab and into the systems that organise work, logistics, and industrial capacity.

What it is

This week’s watch is “What does Meta actually do now?”

At one level, it is a brisk explainer on how Facebook became Meta, and how the company moved from a social platform into a sprawling corporate structure built around Instagram, WhatsApp, ads, hardware, AI, and a still-unresolved metaverse legacy. The video traces the arc from Facebook’s early growth and scandals through the 2021 rebrand, the collapse of the original metaverse narrative, and Meta’s current push into AI, smart glasses, and ever larger infrastructure spending.

What makes it useful is that it is not really asking what Meta says it does. It is asking what the company actually is once the branding falls away.

What stood out

What stood out is how little the underlying business model has changed, even as the narrative around it keeps shifting.

Again and again, the people interviewed in the video come back to the same point: Meta still makes its money primarily by selling attention through Facebook and Instagram. The rebrand, the metaverse, the hardware, the glasses, the AI push. These all sit on top of that engine rather than replacing it. That matters because it helps explain why the company can absorb enormous losses in one area while continuing to scale another. The family of apps still throws off enough revenue to fund very large bets.

The second thing that stood out was the way AI is framed internally. The video suggests Meta’s AI push is not only about launching new products. It is also about avoiding dependence on other companies’ foundational models, in much the same way Meta historically resented being dependent on Apple and Google’s app stores. That is a useful lens. AI begins to look less like a feature race and more like an attempt to own the next platform layer before someone else does.

There is also a darker thread running through it. The video ties Meta’s current AI expansion to internal employee tracking, workplace tension, layoffs, and growing criticism around addictive design and children’s harm. That combination matters. It suggests the company is not just extending its technical reach. It is intensifying the systems around work, attention, and behaviour at the same time.

Why it lingers

It lingers because it clarifies something that can otherwise get lost in the noise.

Meta is often discussed as if it keeps reinventing itself. Social network. Metaverse company. AI company. Hardware company. But the video suggests something more consistent underneath all of that. Meta remains, at its core, a company that builds technologies to capture attention, make that attention more measurable, and turn it into revenue. The surrounding strategies change. The centre holds.

That feels useful this week because the newsletter is circling the question of how platform power is evolving rather than disappearing. If childhood is becoming a central site where platform legitimacy is tested, then it matters that the underlying business incentives remain so stable. A company can change its name, its product mix, and its preferred future. It is harder to change the logic that funds it.

That may be the real reason the video lingers.

It makes Meta feel less like a sequence of pivots and more like a machine searching for its next durable surface.

Digital assets now sit less as an idea and more as infrastructure in progress. As physical and digital life continue to converge, money and assets are doing the same. What was once framed as “crypto” is increasingly showing up as rails, balance sheets, and policy conversations.

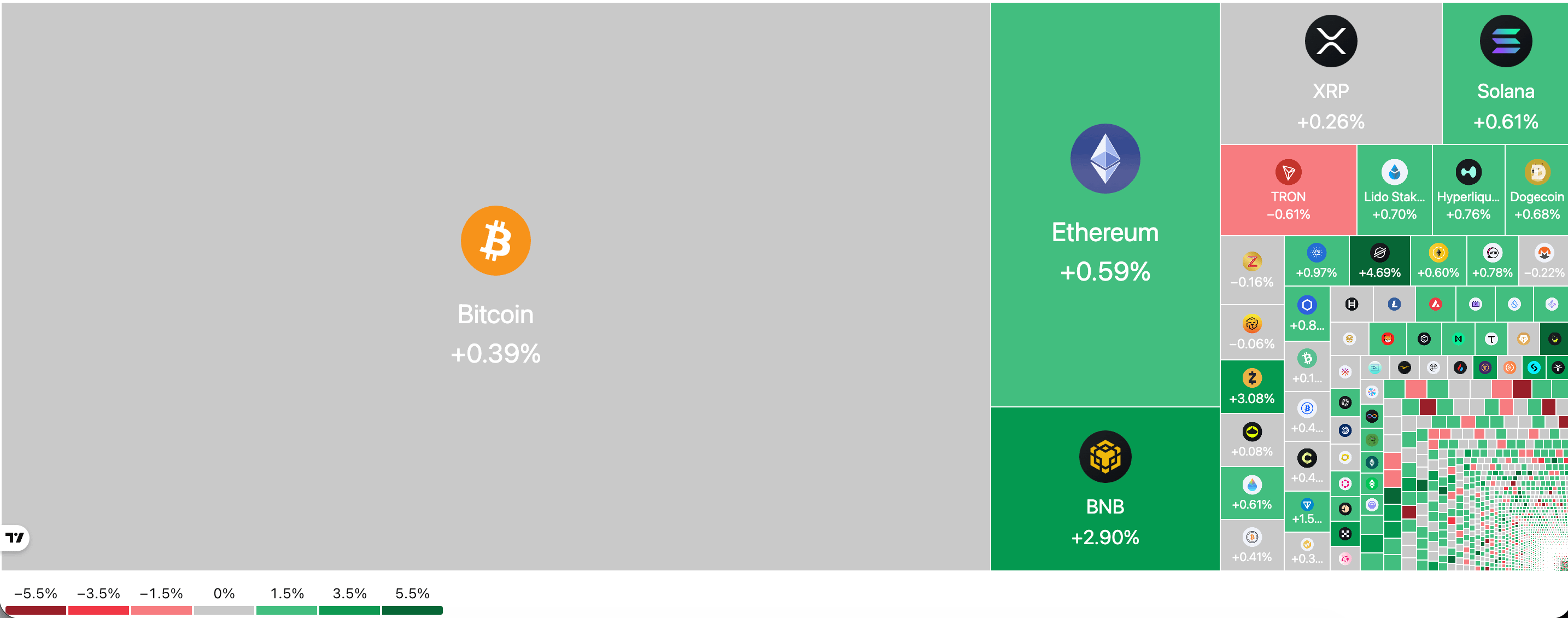

🔥🗺️Heat map shows the 7 day change in price (red down, green up) and block size is market cap.

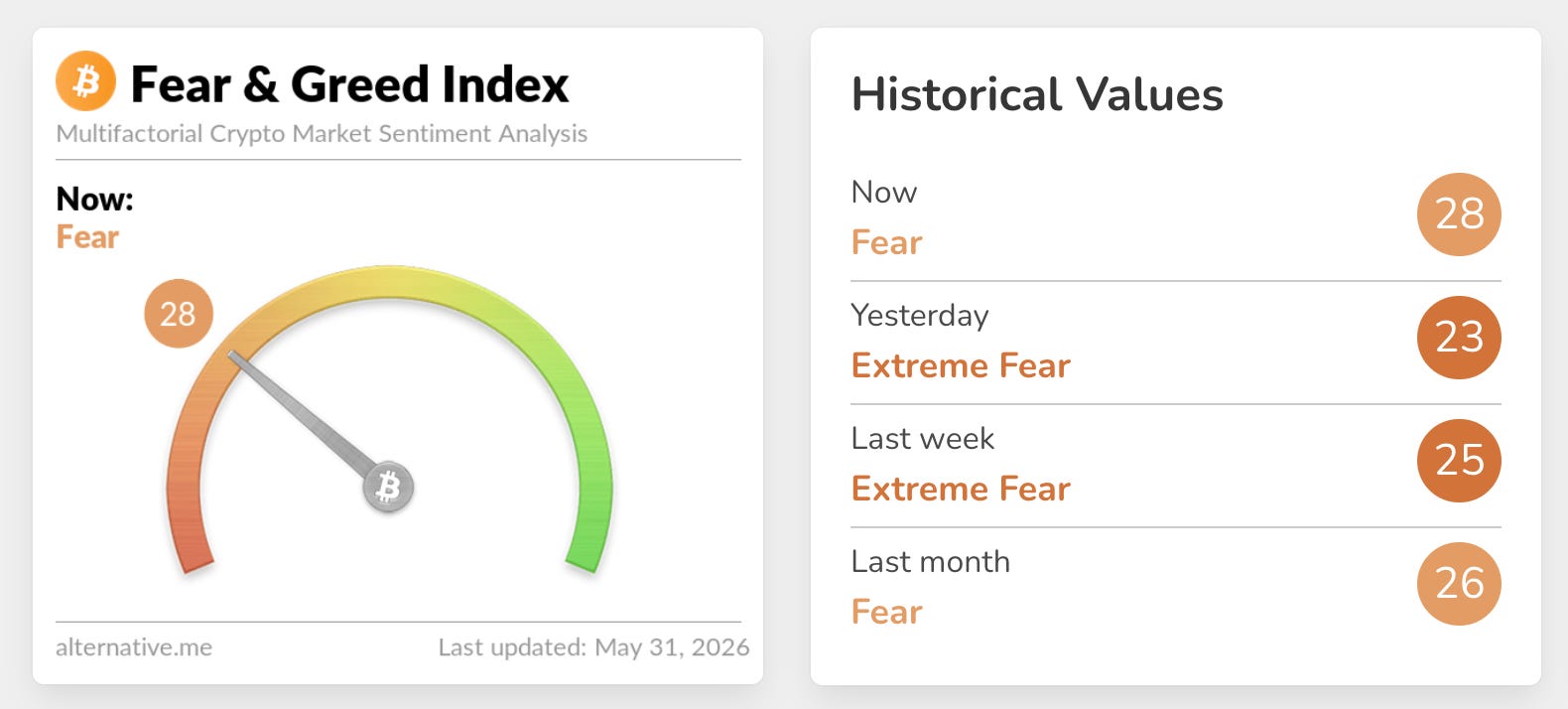

🎭 Crypto Fear and Greed Index is an insight into the underlying psychological forces that drive the market’s volatility. Sentiment reveals itself across various channels—from social media activity to Google search trends—and when analysed alongside market data, these signals provide meaningful insight into the prevailing investment climate. The Fear & Greed Index aggregates these inputs, assigning weighted value to each, and distils them into a single, unified score

This section captures developments at the edge of digital systems. New interfaces, tools, and capabilities that feel early, unfinished, or slightly ahead of their moment. I’m less interested in what’s impressive today and more interested in what might quietly reshape how people work, coordinate, and interact over time.

Space is starting to sound less like a launch story and more like a sovereignty industry.

For years, the public imagination around space has been dominated by spectacle. A rocket lifts off. A constellation is announced. A billionaire gestures toward Mars. What stood out this week was something quieter and, in some ways, more consequential. Reuters reported that Schaeffler has signed a memorandum of understanding with Spire Global to jointly develop space hardware and satellite platforms in Europe, with applications in defence, weather, and security. Schaeffler said the strategic goal is to build a European sovereign space hardware and mission business by the end of the decade, targeting about €250 million in revenue by 2030.

That matters because it shifts the frame away from missions and toward the industrial base underneath them. This is not being pitched as a moonshot. It is being pitched as a supply-chain and manufacturing opportunity. Reuters noted that Spire has capacity to produce 300 to 400 satellites annually across facilities in the United States and Europe. The Schaeffler release goes further, saying the two companies intend to secure and scale supply chains for critical spacecraft subsystems and explore industrialised satellite bus platforms. That is not demo language. It is production language.

The sovereignty angle makes the story more interesting still. The partnership is explicitly framed around building a self-reliant European space-industrial base, industrialised in Germany, flight-proven in orbit, and deployable at scale for defence, weather, civil security, and critical-infrastructure missions. In other words, the frontier here is not only technical capability. It is the question of whether Europe can own more of the hardware, mission architecture, and manufacturing capacity behind systems it increasingly sees as strategic.

That feels directionally important because space is no longer just a communications story. It is becoming part of the sovereignty stack. Weather intelligence. Defence applications. Critical infrastructure. Environmental sensing. Once those functions begin to matter politically, the origin of the hardware starts to matter too. A satellite platform is no longer only a piece of engineering. It becomes part of a broader argument about dependence, security, and industrial resilience.

This may be the useful signal from the field. Frontier technologies often become real twice. First as a vision. Then as a manufacturing category. The second moment is easier to miss because it is less cinematic. But it is usually the one that lasts. What Schaeffler and Spire suggest is that Europe is beginning to treat space less as a downstream service and more as a strategic industrial capability that needs to be built, supplied, and scaled closer to home.

“We tend to meet any new situation by reorganising, and a wonderful method it can be for creating the illusion of progress while producing confusion, inefficiency and demoralisation.”

Charlton Ogburn Jr.

Charlton Ogburn Jr. was an American journalist, writer, and military historian with a sharp eye for the gap between institutional performance and institutional theatre. He understood that organisations under pressure often respond first with movement rather than clarity. New structures. New language. New reporting lines. Plenty of visible activity, but not always much resolution. That is what makes the line feel so durable. Reorganisation can look like momentum even when it mostly rearranges the confusion. This week’s stories sit close to that tension. Systems under pressure do not just reveal what they can do. They reveal how easily motion can be mistaken for progress.