Field Notes Week 176/520: Russia and the Quiet Shutdown

These notes are shaped by what I’m seeing, building, and discussing as our physical and digital lives continue to converge.

Welcome to this week’s Field Notes, a 10-year project of mine documenting humankind’s digital transition from the field. These notes are shaped by what I’m seeing, building, and discussing as our physical and digital lives continue to converge.

- Ryan

(Connect with me on LinkedIn)

News is surface-level. Signals live underneath. This section captures developments that hint at deeper shifts in how digital systems are being built, governed, and adopted — often before they’re obvious in the mainstream narrative.

Three stories this week pointed to the same underlying condition.

Infrastructure is becoming more selective. Not just in what it connects, but in who gets to build it, who gets to access it, and what kinds of dependency it quietly creates. In Europe, telecom security is hardening into industrial policy. In Russia, connectivity is becoming a source of daily economic friction. In the semiconductor market, memory capacity is starting to behave less like supply and more like something that has to be reserved in advance.

Europe is turning telecom security into industrial policy

Reuters reported on 4 May that the European Commission recommended member states exclude Huawei and ZTE equipment from connectivity infrastructure. Reuters also said proposed cybersecurity rules would give the EU more power to ban gear from suppliers deemed high risk, and that China warned of possible countermeasures in response.

What stood out is that this is no longer being framed as a narrow security issue. Procurement starts to look like policy. Infrastructure choices start to carry geopolitical meaning. The physical layer of the network is being treated less as neutral utility and more as a site of political trust.

That feels directionally important because the network only appears apolitical when everyone agrees on who gets to build it. Once those assumptions break, resilience, sovereignty, and vendor choice become harder to separate. Europe is not just trying to secure the network. It is trying to decide what kind of dependency it is still willing to tolerate.

Russia’s internet crackdown is becoming everyday economic drag

Reuters reported on 8 May that Russia’s restrictions on Telegram, curbs on VPNs, and repeated mobile internet shutdowns are disrupting businesses across the country and putting billions of dollars in digital sales at risk. The report said around 2.9 million small firms and more than 14 million self-employed people depend on online messaging for business, while digital sales in Russia reached about $153.74 billion in 2025.

What stood out here is the texture of the damage. Not a dramatic blackout. Not a total collapse. Something slower and more corrosive. Connectivity becomes conditional, and once that happens the cost appears everywhere at once: delayed transactions, lost sales, broken messaging chains, less certainty about whether the system will be available when needed.

That is a useful signal because it shows what happens when the internet stops behaving like background infrastructure and starts behaving like a managed privilege. The effect is not only political. It is commercial and administrative. A business environment built on routine digital assumptions begins to accumulate friction faster than most firms can adapt.

Memory chips are starting to behave like reservation infrastructure

Reuters reported on 7 May that SK Hynix is receiving unprecedented offers from major tech firms seeking to help fund new production lines and expensive manufacturing equipment in exchange for more secure access to memory chip supply. Reuters said there is currently no spare chip manufacturing capacity and that customers are increasingly using long-term contracts and prepayments to secure future output.

What stood out is the shift in market logic. This is no longer only a question of buying what is available when you need it. Companies are trying to reserve future production before it exists. In other words, memory is moving closer to an allocation model. Capacity itself becomes strategic, and access to that capacity becomes something worth underwriting in advance.

That matters because semiconductors increasingly sit underneath everything else. Once customers start funding fabrication capacity directly, the chip market begins to look less like a normal supply chain and more like infrastructure finance. The risk is no longer just shortage. It is exclusion from the next round of capacity.

What stood out

Taken together, these stories suggest that infrastructure is becoming less open by default.

Europe is narrowing who can build the network. Russia is narrowing how reliably the network can be used. The memory market is narrowing who can count on future supply without prior commitments. Different sectors, different pressures, same direction. Systems that once looked broad and universal are beginning to reveal their gates.

What it is

This week’s watch is "Inside Russia: Putin’s internet shutdown explained” from The Global Story.

The episode looks at Russia’s tightening grip on the digital environment and how that control now extends well beyond protest or dissident media. The conversation between Asma Khalid and Steve Rosenberg traces a longer arc: from Putin’s early consolidation of television and traditional media to the present focus on messaging apps, VPNs, and mobile internet access. What emerges is not just a story about censorship. It is a story about the internet being reworked as a managed system.

What stood out

What stood out was the mundanity of the disruption. The episode breaks Russian control into three main mechanisms: restrictions on platforms like WhatsApp and Telegram, the ongoing attempt to block VPNs, and intermittent mobile internet shutdowns. None of that sounds especially novel on its own. But Rosenberg’s account of living through a three-week mobile internet blackout in Moscow makes the effects much clearer. Navigation stops working properly. Payments become harder. Messaging becomes unreliable. Ordinary routines begin to fray.

That felt important because it shifts the story away from abstract ideas like digital repression and back toward lived conditions. The internet is easy to treat as something political only when it disappears completely. This video shows something more common and probably more revealing: a network that still exists, but no longer behaves like dependable infrastructure.

Why it lingers

It lingers because it connects closely to one of the deeper signals in this week’s issue. When connectivity becomes conditional, the damage is not limited to dissent or journalism. It spreads into commerce, administration, and daily life. Small businesses cannot rely on customers reaching them. Payments become more fragile. Logistics and coordination grow less certain. The system still functions, but with more drag built into it.

That makes the Russian story useful beyond Russia. It shows what happens when a network stops being a background utility and starts behaving like a privilege granted in narrower terms. Once that shift begins, the costs accumulate quietly, then everywhere at once.

Digital assets now sit less as an idea and more as infrastructure in progress. As physical and digital life continue to converge, money and assets are doing the same. What was once framed as “crypto” is increasingly showing up as rails, balance sheets, and policy conversations.

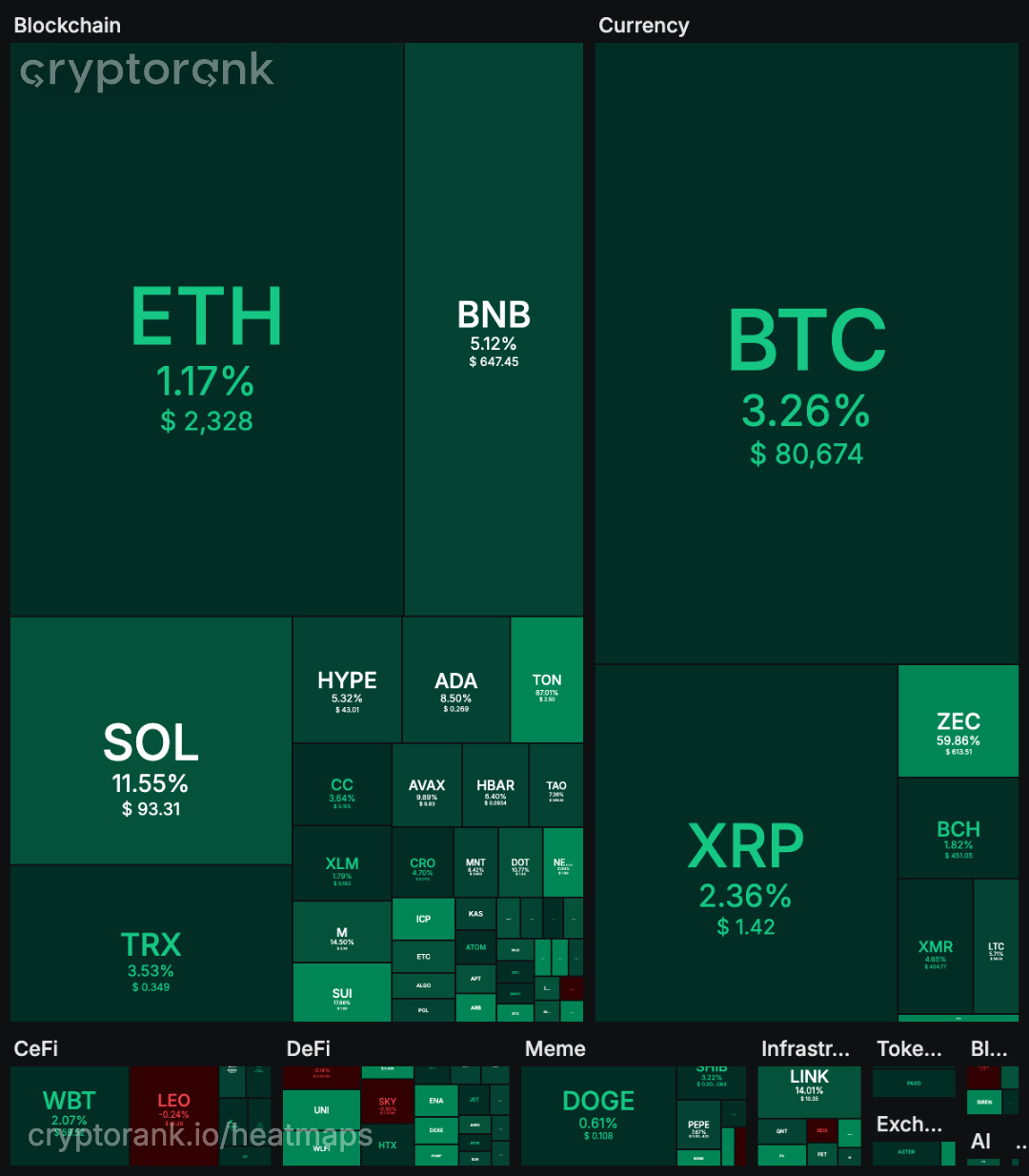

Bitcoin is up modestly over the last 7 days and is trading around $80.4k now. Over that stretch it briefly reached a three-month high before consolidating, with Reuters noting it had topped $80,000 as broader markets responded to tariff relief headlines and a softer dollar.

The main driver appears to be a mix of macro risk sentiment rather than a crypto-specific catalyst. Reuters linked the move to hopes around a U.S.-Iran deal, a weaker dollar, and broader gains in risk assets, while also noting that tariff rulings and equity strength helped lift sentiment across markets.

The move still sits inside a more fragile backdrop. Reuters reported this week that bitcoin remains down about 7% in 2026, weighed by uncertainty over Fed policy, Middle East tensions, and broader market turbulence, even as institutional involvement keeps expanding. So the last 7 days look more like a relief rally within a still macro-driven market than a clean new regime shift.

🔥🗺️Heat map shows the 7 day change in price (red down, green up) and block size is market cap.

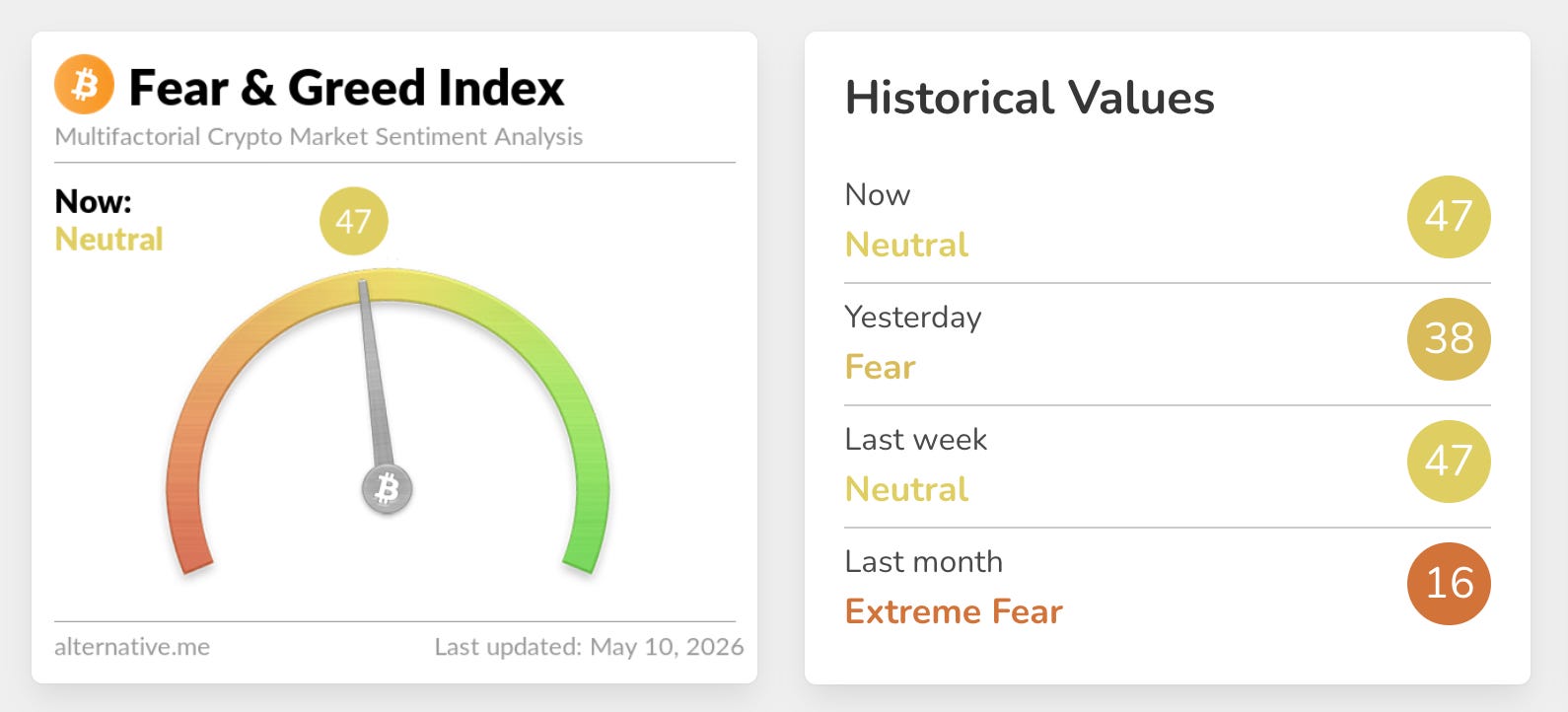

🎭 Crypto Fear and Greed Index is an insight into the underlying psychological forces that drive the market’s volatility. Sentiment reveals itself across various channels—from social media activity to Google search trends—and when analysed alongside market data, these signals provide meaningful insight into the prevailing investment climate. The Fear & Greed Index aggregates these inputs, assigning weighted value to each, and distils them into a single, unified score

.

This section captures developments at the edge of digital systems. New interfaces, tools, and capabilities that feel early, unfinished, or slightly ahead of their moment. I’m less interested in what’s impressive today and more interested in what might quietly reshape how people work, coordinate, and interact over time.

Humanoid robotics is starting to sound less like spectacle and more like procurement.

For a long time, the category has been narrated through demos. A robot walks. A robot dances. A robot folds a shirt, badly, and the clip circulates anyway. Useful theatre, but still theatre. What stood out this week was a change in language. Reuters reported that Schaeffler expects its humanoid robotics business to build an order book in the three-digit million euro range by 2030. The company says it is already working with around 45 robotics entities worldwide and has five customer contracts, with major clients in China and the United States (Source)

That matters because it shifts the frame from possibility to market structure. Schaeffler is not selling a humanoid robot dream in the abstract. It is talking about actuators, strain wave gears, and the component layer that sits underneath the machines. Reuters says the company expects at least 1 million humanoid robots to be produced globally between 2026 and 2030, estimates it can address about half of the materials demand in that sector, and hopes to capture about 10% of that addressable market. That is order-book language. Supplier language. Industrial language.

A second Reuters story pushed the same theme from a different direction. French startup Genesis AI unveiled a general robotics model called GENE-26.5 alongside a highly dexterous robotic hand aimed at sectors such as automotive, electronics, pharmaceuticals, and logistics. Reuters reported that the company is already in advanced talks with clients in France, Germany, and Italy, even if it has not yet named them publicly.

What stood out there was not just the model, but the target market. The hand is being positioned for precise industrial work rather than consumer theatre. Reuters described demonstrations including chopping tomatoes, cracking eggs, solving a Rubik’s Cube, and playing piano, but the more important point was where Genesis says the system is meant to land: in production environments where dexterity and repeatability matter economically. The company has also raised $105 million in what Reuters described as one of France’s largest seed rounds, which suggests investors are starting to treat robotics not simply as a moonshot category, but as an infrastructure layer for European industry.

This feels directionally important. Not because humanoids are suddenly solved. They are not. The category still carries the usual uncertainty around cost, reliability, integration, and what proportion of human work can actually be standardised into machine motion. But the tone is changing. Less “watch this robot do a trick.” More “how large could the supply chain become if this category hardens.”

That may be the useful signal from the field. Frontier technologies tend to become real twice. First as demonstration. Then as procurement. The second moment is quieter, but usually more important. It is when companies stop asking whether the technology is impressive and start asking whether they should reserve capacity, redesign workflows, or build around it. Humanoid robotics still feels early. But it is beginning to attract the language of industrial planning, and that usually means the system underneath the demo is starting to form.

“What we call progress consists in coordinating ideas with realities.”

Alfred Korzybski

Alfred Korzybski was a Polish-born American scientist and philosopher best known as the founder of general semantics, a discipline concerned with how language, abstraction, and human perception shape what we take to be reality. He was born in Warsaw in 1879, studied engineering, served in the Russian army’s intelligence department during World War I, and later remained in North America, eventually becoming a U.S. citizen. Britannica notes that his major work was Science and Sanity (1933), while the Institute of General Semantics, which he founded in 1938, still describes his work as applying scientific thinking and language awareness to how people evaluate the world.

What makes Korzybski useful is that he was not just interested in words. He was interested in the gap between what is happening and how we represent what is happening. That is where his most famous line, “The map is not the territory,” comes from. The point is not merely that maps can be incomplete. It is that all models, labels, categories, and descriptions are abstractions. They help us navigate reality, but they are never reality itself. That idea sits underneath much of general semantics, which was meant to improve habits of evaluation by reminding people that language can conceal as much as it reveals. Britannica describes general semantics as a system aimed at improving humanity’s ability to transmit ideas accurately and develop better habits of evaluation.