Field Notes Week 175/520: BYD and the New Charging Logic

These notes are shaped by what I’m seeing, building, and discussing as our physical and digital lives continue to converge.

Welcome to this week’s Field Notes, a 10-year project of mine documenting humankind’s digital transition from the field. These notes are shaped by what I’m seeing, building, and discussing as our physical and digital lives continue to converge.

- Ryan

(Connect with me on LinkedIn)

News is surface-level. Signals live underneath. This section captures developments that hint at deeper shifts in how digital systems are being built, governed, and adopted — often before they’re obvious in the mainstream narrative.

Two stories this week sat far apart on the surface.

One is about satellites. The other is about batteries. But both point to the same condition: industrial competition is shifting away from products alone and toward the ecosystems that surround them. A space sector begins to look more durable when it becomes a place. An EV market becomes harder to win when the contest is no longer just range, but charging time and charging infrastructure. (Reuters)

Beijing is building a place for commercial space

Reuters reported on 18 April that Beijing is set to complete the core area of a new “Satellite Town” in the second half of 2026, creating a dedicated hub for satellite manufacturers and operators. The project arrives as China’s commercial space sector expands quickly, with the report noting that more than 60% of the country’s launches are now commercial and that many firms are preparing to go public. Reuters also said the next phase of growth is expected to centre on low-Earth-orbit constellations, satellite internet, space-based computing, and integrated 6G systems.

What stood out is that this is not just a sector story. It is a clustering story. Satellite Town is meant to bring talent, capital, technology, and supply chains into closer contact, which is usually what happens when an industry begins to move from frontier status toward something more repeatable. Space is still often framed as launch spectacle. This looks more like industrial policy.

The useful signal is that commercial space is becoming infrastructural. Not only rockets and payloads, but a physical geography of support, financing, manufacturing, and integration. When a government starts building a town around a category, it is making a long-duration bet that the value will sit not just in the objects launched upward, but in the economic system built around them on the ground.

BYD wants charging time to become the new argument

Reuters reported today that BYD says its second-generation batteries can charge from 20% to 97% in under 12 minutes, even at minus 20 degrees Celsius, while delivering a range of 777 kilometres. Reuters also reported that BYD plans to build around 20,000 flash-charging stations in China and 6,000 overseas within a year, as it tries to win over drivers who still hesitate to switch from petrol because of charging time and range anxiety. (Reuters)

What stood out is how the pitch has changed. For years, battery competition was framed mainly through range. Now the more interesting variable may be time. If charging becomes fast enough, then one of the last psychological barriers to EV adoption begins to weaken. Reuters quotes BYD executive vice president Stella Li saying flash charging “solves the last barrier for EV adoption” and allows BYD to “compete with the gas market.” That is not just a chemistry claim. It is a behavioural one.

The deeper point is that batteries are no longer only battery stories. They are infrastructure stories. BYD is not just improving a cell. It is pairing the technical advance with a buildout plan for charging stations, which suggests the real contest is becoming system-level: battery performance, network availability, user confidence, and habit change all moving together. That feels directionally important because it is usually at that level that adoption stops being aspirational and starts becoming ordinary.

What stood out

Taken together, these stories suggest that the next phase of technological competition is becoming more territorial and more operational. China’s space sector is being organised as a place. China’s EV sector is being pushed toward a world where charging speed and charging presence matter as much as the vehicle itself. In both cases, the visible product still matters. But the quieter signal sits underneath it: durable advantage increasingly comes from the surrounding system.

What it is

This week’s watch is an episode of The Everything Electric Podcast featuring Robert Llewellyn in conversation with Sajid Hasan, Chief Product Officer for BYD Australia and New Zealand.

On the surface, it is a discussion about BYD’s rapid rise, battery technology, charging speed, and the company’s position in Australia. Underneath that, it is really about something larger: how an electric vehicle company starts to behave less like a carmaker and more like an energy and infrastructure company. The conversation moves from the LFP Blade Battery and DMO Super Hybrid platform to 1-megawatt flash charging, vehicle-to-grid trials, and Australia’s role as a proving ground for what comes next.

What stood out

What stood out is how system-level the story has become.

BYD is presented not just as a manufacturer of vehicles, but as a vertically integrated company with control across batteries, semiconductors, and supply chains. That changes the shape of the discussion. The car becomes one expression of a larger industrial stack. Sajid Hasan describes BYD as a battery company that started making cars, which feels like a more revealing way to read the company than the usual automotive framing.

The second thing that stood out was the emphasis on charging time and energy flow rather than simple range. The claim that BYD’s 1-megawatt flash chargers can add 400 kilometres in five minutes shifts the conversation away from the familiar EV question of whether batteries last long enough. It points instead to a future where the more relevant question is how quickly electricity can move, where it can move, and what kind of infrastructure is required to make that feel ordinary.

Then there is the Australian angle. Hasan frames Australia as a right-hand-drive export market, a competitive proving ground, and a place where solar adoption, long driving distances, and consumer price sensitivity make it unusually useful for testing the future of electric mobility. That felt important. Markets like this do not just receive technology. They help shape which versions of it survive.

Why it lingers

It lingers because it suggests the EV transition is entering a different phase.

For years, electric vehicles were discussed mainly as a substitution story: one drivetrain replacing another. This conversation makes the category feel broader than that. Batteries are not just storage. Cars are not just transport. Charging is not just refuelling. Once V2G enters the frame and EVs are described as mobile power plants, the edges between transport, household energy, and grid infrastructure begin to blur.

Digital assets now sit less as an idea and more as infrastructure in progress. As physical and digital life continue to converge, money and assets are doing the same. What was once framed as “crypto” is increasingly showing up as rails, balance sheets, and policy conversations.

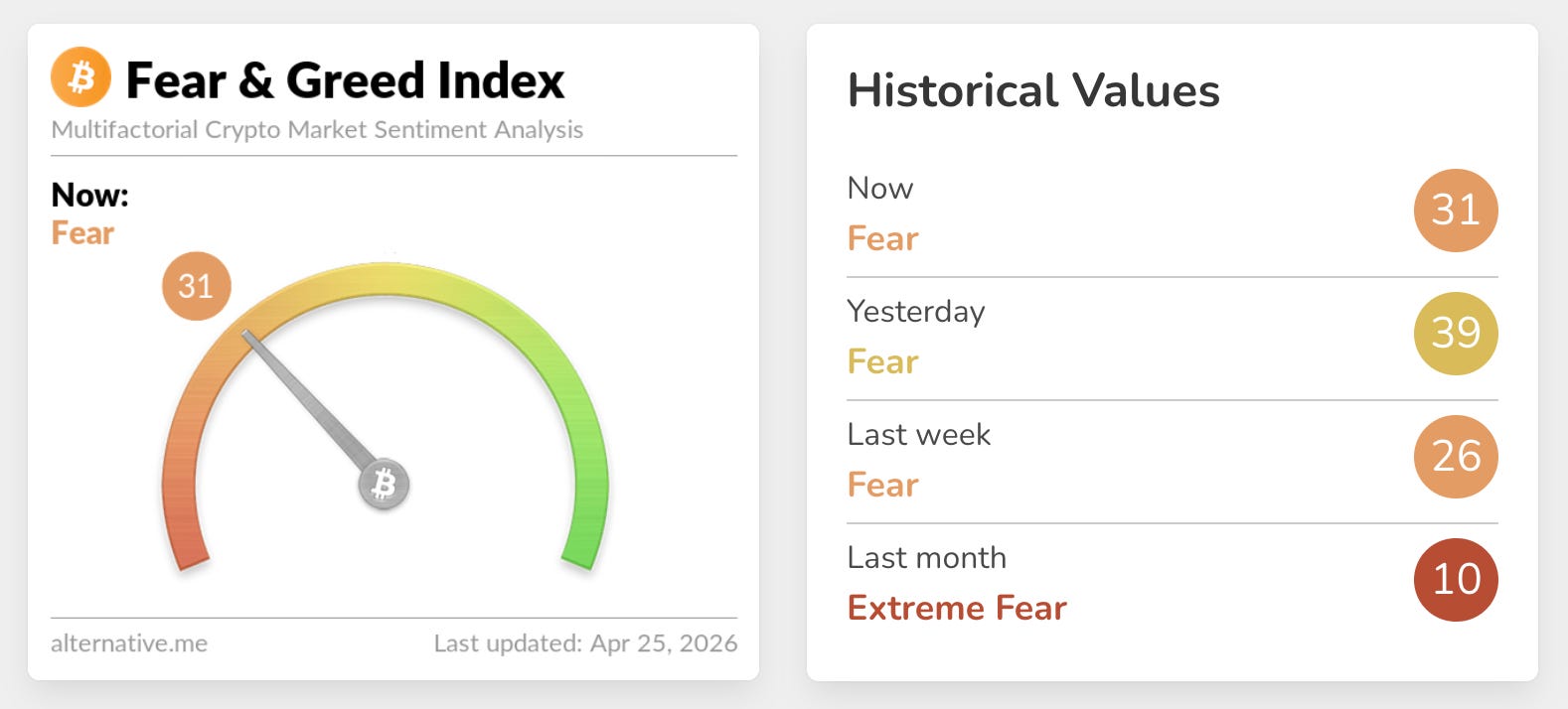

🔥🗺️Heat map shows the 7 day change in price (red down, green up) and block size is market cap.

🎭 Crypto Fear and Greed Index is an insight into the underlying psychological forces that drive the market’s volatility. Sentiment reveals itself across various channels—from social media activity to Google search trends—and when analysed alongside market data, these signals provide meaningful insight into the prevailing investment climate. The Fear & Greed Index aggregates these inputs, assigning weighted value to each, and distils them into a single, unified score

.

This section captures developments at the edge of digital systems. New interfaces, tools, and capabilities that feel early, unfinished, or slightly ahead of their moment. I’m less interested in what’s impressive today and more interested in what might quietly reshape how people work, coordinate, and interact over time.

Direct-to-device satellites are starting to look less like a backup and more like a new layer of connectivity. For years, satellite links sat mostly at the edge of the system. Emergency use. Remote coverage. Specialist hardware. A signal of last resort. That framing is getting harder to maintain. The ITU said this month that direct-to-device satellite systems are moving beyond niche use cases, with multiple technical approaches now trying to connect ordinary phones directly from space rather than relying only on terrestrial towers. Its argument is that this is no longer just a rural-coverage story. It is becoming a broader question of how the world stays connected when the ground network is absent, weak, or commercially uneconomic. (Reuters)

What stood out is how quickly the market structure around this is filling in. Reuters noted last week that satellite internet is expanding well beyond remote households into aviation, shipping, defence, emergency messaging, and direct-to-phone services. Light Reading reported that mobile operators are now teaming up with satellite players “in their droves,” increasingly treating direct-to-device capability as an extension of the 5G footprint rather than a separate category entirely. That changes the posture of the technology. It stops looking like an exotic add-on and starts looking like a complementary network layer.

The more interesting shift is not technical alone. It is architectural.

Once a normal handset can fall back to a satellite layer, the old assumptions about network boundaries start to loosen. Coverage no longer maps as neatly onto national telecom infrastructure. Resilience starts to depend on orbital systems, launch cadence, spectrum access, and the agreements between mobile operators and satellite firms. In that world, connectivity becomes a more hybrid stack. Part tower. Part orbit. Part policy. (Light Reading)

This also reframes the space story. The Reuters report on China’s emerging “Satellite Town” already suggested that commercial space is becoming more infrastructural and less spectacular. Direct-to-device services make that even clearer. The point is not only to launch satellites. It is to build an alternative communications layer that can sit quietly behind everyday behaviour. When that works well, users may barely notice which part of the stack they are on.

Still unresolved is what this does to control.

Because once connectivity becomes multi-layered, sovereignty becomes harder to read. The regulatory questions do not disappear. They multiply. Who governs the traffic. Which standards apply. What parity should exist between terrestrial and orbital providers. The GSMA warned in March that direct-to-user LEO services need clearer and more harmonised regulatory treatment if they are to scale without creating uneven obligations across providers. That is usually the moment when a frontier technology starts becoming real: when the legal architecture begins trying to catch up with the network architecture.

The future of connectivity may not arrive as a single new network. It may arrive as a quieter change in which phones simply expect the sky to be part of the system.

“Energy is the universal currency.”

Vaclav Smil

Vaclav Smil is a Czech-Canadian scientist and policy analyst who spent decades at the University of Manitoba and has written extensively on energy, materials, food systems, and the physical foundations of modern civilisation. The MIT Press describes him as Distinguished Professor Emeritus at the University of Manitoba and notes that his work consistently returns to the long arc of how energy shapes society. The line itself comes from Smil’s framing in Energy and Civilization, where he argues that “Energy is the only universal currency; it is necessary for getting anything done.” That is why the quote works so well here. It reduces a complicated week back to a basic condition: beneath batteries, satellites, transport, and infrastructure, the deeper contest is still about how energy is stored, moved, and transformed. (MIT Press)