Field Notes Week 170/520:

These notes are shaped by what I’m seeing, building, and discussing as our physical and digital lives continue to converge.

Welcome to this week’s Field Notes, a 10-year project of mine documenting humankind’s digital transition from the field. These notes are shaped by what I’m seeing, building, and discussing as our physical and digital lives continue to converge.

- Ryan

(Connect with me on LinkedIn)

News is surface-level. Signals live underneath. This section captures developments that hint at deeper shifts in how digital systems are being built, governed, and adopted — often before they’re obvious in the mainstream narrative.

Payments reform is slipping, and regulators are starting to say so

Speaking at an FSB payments summit on 12 March, Andrew Bailey, chair of the Financial Stability Board and governor of the Bank of England, urged governments to push ahead with reforms to international and domestic payment systems. He said progress under the G20-backed roadmap for cross-border payments had been made, but remained uneven, and warned that persistent inefficiencies risk fragmenting the global financial system. (Reuters)

What stands out is the tone. Cross-border payments have been criticised for years for high costs, slow settlement, and weak transparency, yet the reform story still feels incomplete. Reuters notes that the FSB said in October global authorities were set to miss a 2027 target to reduce the average cost of cross-border retail payments to no more than 1%, and to have 75% of wholesale and retail payments credited within an hour. (Reuters)

The signal here is that payments modernisation is no longer just a matter of better rails. It is becoming a coordination problem across jurisdictions, standards, supervision, and data frameworks. Bailey also announced work toward a 2027 review of FSB recommendations on data frameworks and supervision, which suggests the next phase may depend as much on governance and interoperability as on the mechanics of moving money. (Reuters).

I’m watching closely because when core payment reform slips for long enough, the risk is not just inconvenience. It is that fragmentation becomes the default condition, and alternative systems begin to fill the gaps.

Offline payments are moving from contingency planning toward policy design

Reuters reported that Finland, Sweden, Norway, Denmark, and Estonia are rolling out or developing offline card payment systems to ensure consumers can still buy essential goods if internet connections are disrupted. The plans follow repeated damage to critical undersea infrastructure in the Baltic Sea region and growing concern that payments systems could become targets of sabotage or geopolitical pressure. (Reuters)

What stands out is the change in assumption. In Finland, where only around 10% of people use cash as their primary payment method, the payments system is now being treated as a resilience problem, not just a convenience layer. Sweden’s central bank told Reuters it hopes to have a system in place by 1 July 2026 that would allow offline card payments for up to seven days during a disruption, while Norway and Denmark said they have already launched offline electronic payments that they continue to develop. (Reuters)

The signal here is broader than one region. As countries become more dependent on cards, apps, and international data links, payment resilience starts to look like national infrastructure policy. Reuters also notes that Finland’s central bank sees heavy reliance on Visa and Mastercard rails as a vulnerability, and is pursuing a national instant payments system alongside reserve bank accounts that could give people access to savings if their bank cannot operate. (Reuters)

Once digital societies begin designing for interruption, the story is no longer just about faster payments. It is about sovereignty, redundancy, and the return of cash-like resilience inside electronic systems.

What it is

Here is an interview I recently did on stablecoins, AI agents, and why digital money infrastructure is starting to matter beyond crypto itself. We covered NewMoney, the rise of non-USD stablecoins, and why payments, FX, and settlement may look very different in a more agentic economy.

What stood out

One point feels especially important. If AI agents are earning, negotiating, investing, and moving capital on behalf of people or firms, they will not work well with systems built around bank onboarding, delayed settlement, and expensive cross-border transfers. They need money that moves as fast as they do.

The interview also touches on a second issue that still feels underpriced. If digital finance keeps growing on USD stablecoin rails, smaller economies risk drifting into someone else’s monetary layer by default. That is part of why NewMoney exists. Non-USD stablecoins are not just a product category. They may become part of the infrastructure for retaining monetary relevance in a digital economy.

Why it lingers

Stablecoins are easiest to misunderstand when viewed as another type of crypto or speculative asset. More interesting is to view them as a new operating layer for moving value. Faster settlement. Cleaner FX. Programmable escrow. Assets and money on the same ledger.

That shift still feels early, but it is becoming easier to see where it leads. When money becomes internet-native, the systems built around it start to change as well.

You can learn more about NewMoney at www.getnew.money.

Digital assets now sit less as an idea and more as infrastructure in progress. As physical and digital life continue to converge, money and assets are doing the same. What was once framed as “crypto” is increasingly showing up as rails, balance sheets, and policy conversations.

🔥🗺️Heat map shows the 7 day change in price (red down, green up) and block size is market cap.

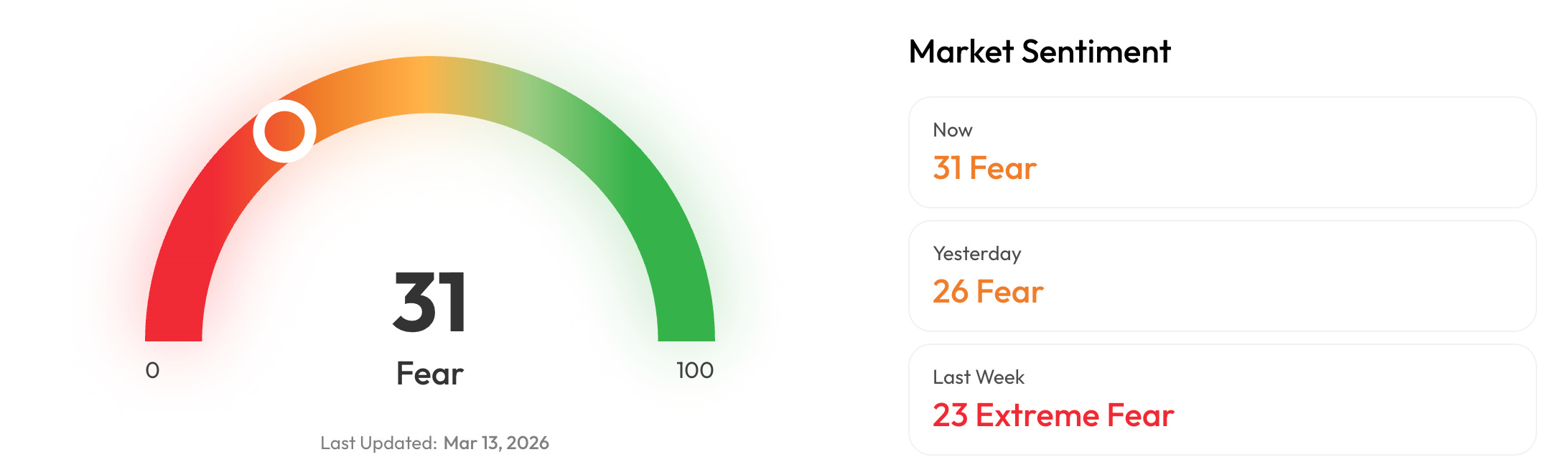

🎭 Crypto Fear and Greed Index is an insight into the underlying psychological forces that drive the market’s volatility. Sentiment reveals itself across various channels—from social media activity to Google search trends—and when analysed alongside market data, these signals provide meaningful insight into the prevailing investment climate. The Fear & Greed Index aggregates these inputs, assigning weighted value to each, and distils them into a single, unified score.

This section captures developments at the edge of digital systems. New interfaces, tools, and capabilities that feel early, unfinished, or slightly ahead of their moment. I’m less interested in what’s impressive today and more interested in what might quietly reshape how people work, coordinate, and interact over time.

A short explainer circulating this week looks at a quiet feature of modern payment systems: the ability to complete transactions even when a device has no internet connection. The video walks through how digital wallets rely on tokenisation and secure hardware to authorise payments offline, a design inherited from the EMV chip standards that underpin modern credit and debit cards. It also touches on emerging approaches, from store-and-forward merchant terminals to experimental systems that transmit payment data through encrypted sound. Source: Offline Digital Payments: How Money Works Without Internet (video explainer).

The deeper signal sits beneath the convenience. As economies move further from physical cash, digital money has to inherit the same reliability that cash once provided. A payment system that only works when networks are stable is fragile by definition. This is why offline capability has become a priority in central bank research into future digital currencies. Surveys by the Bank for International Settlements show almost all central banks now view offline payments as either vital or advantageous to the design of digital money.

The design challenge is subtle. Systems must allow transactions when connectivity is missing while preventing fraud, replay attacks, or double spending once networks reconnect. In practice this pushes trust into hardware, cryptographic tokens, and delayed settlement models. The result is a payment architecture that increasingly assumes intermittent connectivity rather than perfect uptime. In a world where networks can fail, degrade, or be deliberately restricted, the ability for money to keep moving offline becomes less a technical feature and more a condition for resilience and inclusion.

“The future is not a destination, it is a direction.”

Raymond Williams

Raymond Williams was a Welsh cultural theorist, novelist, and one of the founding figures of modern cultural studies. Writing in the mid-20th century, he was interested in how culture, economics, and institutions evolve together over long periods of time. Rather than seeing history as a sequence of clean breaks or inevitable outcomes, Williams focused on the lived process of change. How structures slowly shift as new practices emerge alongside the old.

The line reflects that sensibility. The future is rarely something that arrives fully formed. It is a trajectory shaped by accumulated decisions, incentives, and constraints. Systems do not leap neatly from one state to another. They drift, adapt, and occasionally accelerate.

From the field, that framing feels useful. The task is not to identify the final destination but to notice the direction of travel while it is still forming.