Field Notes Week 167/520: Africa’s layered approach to digital money and identity

These notes are shaped by what I’m seeing, building, and discussing as our physical and digital lives continue to converge.

Welcome to this week’s Field Notes, a 10-year project of mine documenting humankind’s digital transition from the field. These notes are shaped by what I’m seeing, building, and discussing as our physical and digital lives continue to converge.

- Ryan

(Connect with me on LinkedIn)

News is surface-level. Signals live underneath. This section captures developments that hint at deeper shifts in how digital systems are being built, governed, and adopted — often before they’re obvious in the mainstream narrative.

African Union advances cross-border digital ID interoperability amid rising digital asset adoption

The African Union has continued discussions around harmonising digital identity frameworks to improve cross-border recognition of credentials among member states. Rather than proposing a single continental ID, the focus is on interoperability standards that allow national systems to communicate and verify credentials across borders. (Source: African Union digital transformation updates, February 2026.)

This conversation sits alongside Africa’s already significant engagement with digital finance. Several African countries rank among the highest globally for grassroots crypto adoption, driven by remittance flows, currency volatility, and mobile-first payment cultures. According to Chainalysis, multiple Sub-Saharan African economies have consistently placed in the top tier of global crypto adoption indices in recent years. (Source: Chainalysis Global Crypto Adoption Index 2025 edition)

At the same time, central bank experiments have produced mixed results. Nigeria’s Central Bank of Nigeria launched the eNaira in 2021, but uptake has remained limited relative to private stablecoin and peer-to-peer usage. (Source: Central Bank of Nigeria reports; IMF regional digital currency assessments 2025).

What stands out is the layering. Grassroots digital asset adoption has often moved faster than state-backed systems, while public authorities now focus on identity interoperability as a foundation for trade, taxation, and social service delivery. The signal here is not that one model is winning, but that Africa’s digital transition is unfolding across parallel tracks: informal crypto networks, formal CBDC experiments, and now regional identity coordination.

Still early. But when identity standards, mobile payments, and digital assets begin to intersect at continental scale, the question shifts from adoption to integration.

What it is

A news segment on Nigeria’s expansion of its digital identity system, linking biometrics, SIM registration, passports, university exams, and voter enrolment to a single National Identity Number issued by the National Identity Management Commission.

What stood out

The scale of formal invisibility. A large share of the population is without documentation. A state attempting to compress decades of administrative build-out into a digital layer. Identity is not positioned as an optional convenience. It is framed as a prerequisite. Access to services is increasingly routed through a number.

Security concerns are acknowledged, but rollout proceeds regardless. Protection becomes a parallel project, not a precondition.

Why it lingers

Emerging markets are not modernising legacy systems. In many cases, there are no deeply embedded legacy systems to unwind. That absence creates room for architectural jumps. Digital identity can be integrated directly into telecoms, payments, exams, and voting without negotiating layers of analogue history.

In that sense, parts of Africa, Latin America, and Southeast Asia may not be catching up. They may be compressing institutional build-out into a single generational shift. While Western states wrestle with retrofitting fragmented databases and privacy regimes onto ageing infrastructure, newer systems are being designed natively digital.

The question is no longer whether these regions will digitise. It is whether they may ultimately operate more coherently than those who industrialised first.

Digital assets now sit less as an idea and more as infrastructure in progress. As physical and digital life continue to converge, money and assets are doing the same. What was once framed as “crypto” is increasingly showing up as rails, balance sheets, and policy conversations.

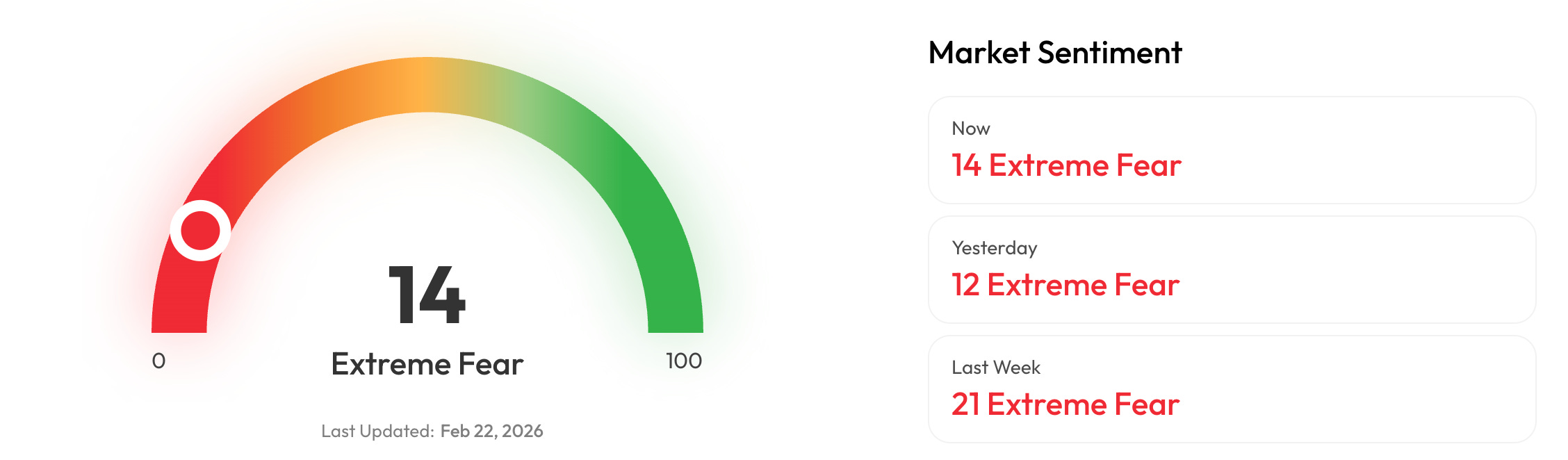

🔥🗺️Heat map shows the 7 day change in price (red down, green up) and block size is market cap.

🎭 Crypto Fear and Greed Index is an insight into the underlying psychological forces that drive the market’s volatility. Sentiment reveals itself across various channels—from social media activity to Google search trends—and when analysed alongside market data, these signals provide meaningful insight into the prevailing investment climate. The Fear & Greed Index aggregates these inputs, assigning weighted value to each, and distils them into a single, unified score.

This section captures developments at the edge of digital systems. New interfaces, tools, and capabilities that feel early, unfinished, or slightly ahead of their moment. I’m less interested in what’s impressive today and more interested in what might quietly reshape how people work, coordinate, and interact over time.

Offline digital identity as infrastructure, not convenience

There has been renewed technical and policy discussion around verifiable credentials that can be checked without live internet access, particularly in humanitarian contexts, border crossings, and low-connectivity regions. Standards bodies and digital identity alliances are increasingly focusing on wallets that can store credentials locally and present them peer-to-peer, with cryptographic verification happening offline.

The frontier signal is subtle. For years, digital ID systems have assumed persistent connectivity to central registries or cloud-based validation endpoints. That assumption holds in dense urban markets, but it breaks quickly in remote regions, disaster zones, or during network disruption. Offline-capable credentials shift the design priority from constant synchronisation to eventual reconciliation.

Over the next five to ten years, this reframes inclusion. If identity can be verified without real-time connectivity, services such as payments, healthcare access, or education enrolment become less dependent on network uptime. But trade-offs emerge. Offline systems must guard against replay attacks, fraud, and double-issuance while preserving privacy. The incentive shifts from central authority to edge security.

The broader implication is behavioural. When identity is portable and locally verifiable, trust moves closer to the individual device rather than a distant database. That decentralisation can expand participation, but it also concentrates responsibility on users and device integrity. The unresolved question is whether resilience and inclusion can scale together without reintroducing new forms of fragility at the edge.

“Institutions are the slowest moving technology.”

Douglass North

Douglass North was an American economist and Nobel Laureate whose work focused on how institutions shape economic performance over long periods of time. Rather than treating growth as purely a function of capital or innovation, he argued that the deeper determinant was the structure of rules, incentives, and enforcement mechanisms within a society. Property rights, contract law, political stability, norms of trust. These were not background conditions. They were the infrastructure.

Calling institutions a technology reframes them. They are designed systems for coordinating behaviour at scale. But unlike software or hardware, they update slowly. Often incrementally. Sometimes reluctantly. Finance makes this visible. Markets can reprice in seconds. Settlement cycles, compliance regimes, and legal definitions of ownership can take decades to adjust. The friction we experience in periods of technological acceleration is often institutional lag, not technical limitation.

From the field, this helps explain the tension between blockchain-based systems and traditional financial infrastructure. The technical layer can change quickly. The institutional layer moves at a different pace. Progress, then, is not just about building new rails. It is about whether the slower technology of institutions is willing, or able, to adapt.